Subprime inqirozi haqida ma'lumot - Subprime crisis background information

Bu maqola kabi yozilgan shaxsiy mulohaza, shaxsiy insho yoki bahsli insho Vikipediya tahrirlovchisining shaxsiy his-tuyg'ularini bayon qiladigan yoki mavzu bo'yicha asl dalillarni keltiradigan. (2013 yil aprel) (Ushbu shablon xabarini qanday va qachon olib tashlashni bilib oling) |

Ushbu maqola haqida ma'lumot beradi ipoteka inqirozi. Unda muhokama qilinadi subprime kreditlash, inqiroz ta'sirida turli xil sub'ektlar ta'sir ko'rsatgan, garovga qo'yilgan mablag'lar, tavakkal turlari va mexanizmlari.

Subprime kreditlash

AQSh Federal depozitlarni sug'urtalash korporatsiyasi (FDIC) subprime qarz oluvchilar va kredit berishni belgilab qo'ydi: "Subprime atamasi qarz oluvchilarning kredit xususiyatlariga taalluqlidir. Subprime qarz oluvchilar odatda zaiflashgan kredit tarixlariga ega bo'lib, ular to'lovlarni kechiktirishni o'z ichiga oladi va ehtimol yanada jiddiy muammolar, masalan, to'lovlar, sud qarorlari va bankrotlik. Shuningdek, ular kredit ballari, qarzdan daromadga nisbati yoki kredit tarixi to'liq bo'lmagan qarz oluvchilarni qamrab olishi mumkin bo'lgan boshqa mezonlarga qarab kamaytirilgan to'lov imkoniyatlarini namoyish qilishi mumkin. kelib chiqishi yoki sotib olinishi .. Bunday kreditlar yuqori xavfga ega sukut bo'yicha asosiy qarz oluvchilarga qarz berishdan ko'ra. "[1] Agar qarz oluvchi kredit xizmatiga (bank yoki boshqa moliyaviy firma) o'z vaqtida ipoteka to'lovlarini to'lashda huquqbuzar bo'lsa, qarz beruvchi ushbu mulkka egalik qilishi mumkin. musodara qilish.

Oddiy tilda umumiy ma'lumot

Quyidagilar AQShning sobiq prezidentidan olingan (ba'zi o'zgartirishlar bilan) Jorj V.Bush 2008 yil 24 sentyabrdagi Xalqqa Murojaat:[2] Boshqa qo'shimchalar keyinchalik maqolada yoki asosiy maqolada keltirilgan.

Bugungi kunda biz guvoh bo'lgan muammolar uzoq vaqt davomida ishlab chiqilgan. O'n yildan ko'proq vaqt davomida AQShga chet eldan sarmoyadorlardan katta miqdordagi pul tushdi. AQSh banklari va moliya institutlariga ushbu katta miqdordagi pul oqimi - past foiz stavkalari bilan birga - amerikaliklar uchun kredit olishni osonlashtirdi. Oson kredit - uydagi qadriyatlar o'sib boraveradi degan noto'g'ri taxmin bilan birlashganda, haddan oshish va noto'g'ri qarorlarga olib keldi.

Ko'pgina ipoteka kreditorlari qarz oluvchilarning to'lov qobiliyatini sinchkovlik bilan tekshirmasdan kreditlarni ma'qulladilar. Ko'plab qarz oluvchilar, keyinchalik uylarini yuqori narxda sotish yoki qayta moliyalashtirishlari mumkin deb o'ylab, imkoniyatlaridan kattaroq kreditlar olishdi. O'tgan o'n yil ichida ham jismoniy shaxslar, ham moliya institutlari qarzdorlik darajasini tarixiy me'yorlarga nisbatan sezilarli darajada oshirdilar.

Uy-joy qadriyatlari haqidagi optimizm, shuningdek, uy qurilishi rivojlanishiga olib keldi. Oxir oqibat yangi uylar soni ularni sotib olishni xohlovchilar sonidan oshib ketdi. Ta'minot talabdan oshib ketishi bilan uy-joy narxi tushib ketdi. Va bu muammo tug'dirdi: tuzatilishlar sodir bo'lgunga qadar uylarini sotish yoki qayta moliyalashtirishni rejalashtirgan, tartibga solinadigan foizli ipoteka kreditlari (ya'ni keyinchalik past ko'tarilganlar), qarz oluvchilar qayta moliyalashga qodir emas edilar. Natijada, ko'plab ipoteka egalari tuzatishlar boshlanganligi sababli defoltni boshladilar.

Ushbu keng tarqalgan defoltlar (va tegishli qarzdorlik) uy-joy bozoridan tashqarida ham ta'sir ko'rsatdi. Uy kreditlari ko'pincha birlashtirilib, "ipoteka bilan ta'minlangan qimmatli qog'ozlar" deb nomlanadigan moliyaviy mahsulotlarga aylantiriladi. Ushbu qimmatli qog'ozlar butun dunyo bo'ylab investorlarga sotilgan. Ko'pgina investorlar ushbu qimmatli qog'ozlarni ishonchli deb hisoblashdi va ularning haqiqiy qiymati to'g'risida bir nechta savol berishdi.

Kredit reyting agentliklari ularga yuqori darajadagi, xavfsiz reytinglarni berdi. Ipoteka kreditlari bilan ta'minlangan etakchi sotuvchilarning ikkitasi edi Fanni Mey va Freddi Mak. Ushbu kompaniyalar kongress tomonidan nizomga olinganligi sababli, ko'pchilik federal hukumat tomonidan kafolatlanganiga ishonishgan. Bu ularga ulkan miqdordagi mablag'ni qarz olish, bozorni shubhali investitsiyalar uchun yoqish va moliya tizimini xavf ostiga qo'yishga imkon berdi.

Uy-joy bozoridagi pasayish AQSh iqtisodiyoti bo'ylab domino effektini o'rnatdi. Uy-joy qiymatlari pasayganda va ipoteka to'lovining to'lanadigan stavkalari ko'payganida, qarz oluvchilar ipoteka kreditlarini to'lamadilar. Dunyo miqyosida ipoteka bilan ta'minlangan qimmatli qog'ozlarga ega bo'lgan investorlar (shu jumladan, ularni yaratgan va o'zaro savdo qilgan ko'plab banklar) jiddiy zarar ko'rishni boshladilar. Ko'p o'tmay, ushbu qimmatli qog'ozlar shu qadar ishonchsiz bo'lib qoldiki, ular sotib olinmaydi yoki sotilmaydi.

Kabi investitsiya banklari Bear Stearns va Lehman birodarlar sotish mumkin bo'lmagan katta miqdordagi mol-mulk bilan o'ralgan holda o'zlarini topdilar. Ular zudlik bilan majburiyatlarini bajarish uchun zarur bo'lgan pullarni tugatdilar va yaqinda qulashga duch kelishdi. Boshqa banklar jiddiy moliyaviy muammolarga duch kelishdi. Ushbu banklar o'z pullarini ushlab tura boshladilar va kredit berish qurib qoldi va Amerika moliya tizimining mexanizmlari to'xtab qola boshladi.

Prekursor, "Subprime I"

Garchi subprime ipoteka inqiroziga oid ko'pgina ma'lumotlarda 2008 yilda boshlangan moliyaviy inqiroz va keyingi tanazzulga olib kelgan voqealar va sharoitlar nazarda tutilgan bo'lsa-da, 1990 yillarning o'rtalarida va oxirlarida, ba'zida "Subprime I" deb nomlangan juda kichik pufak va qulash sodir bo'ldi.[3] yoki "Subprime 1.0".[4] Bu 1999 yilda ipoteka subyekti sekyuritizatsiyasi stavkasi 1998 yildagi 55,1% dan 1999 yildagi 37,4% gacha tushganda tugagan. Keyingi ikki yil ichida 1998 yil Rossiya moliyaviy inqirozi, "o'nta" o'nta qarz beruvchilarning sakkiztasi "bankrotligini e'lon qildi, faoliyatini to'xtatdi yoki kuchliroq firmalarga sotildi."[5]

Aytishlaricha, inqiroz "klassik pufakchaning barcha nishonlariga" qimmatli qog'ozlar narxlarining ko'tarilishidan ishtiyoq bilan eskirgan ishbilarmonlik amaliyoti va kompaniyalarning daromadlari barqaror bo'ladimi degan xavotir o'rnini bosdi. Kreditlar ularni qaytarib berishga qodir bo'lmagan qarz oluvchilarga berildi. Ikkilamchi ipoteka kompaniyalari kutilmagan tarzda hisobdan chiqarishni boshladilar, chunki ipoteka kreditlari past foizli stavkalar bilan qayta moliyalashtirildi. Hisobotdagi foydaning aksariyati xayoliy bo'lib chiqdi va Famco kabi kompaniyalar ish boshladi. Bankrotlik bilan bir qatorda subprime sanoatini yirtqich qarz berishda ayblagan iste'molchilar advokatlarining da'volari va shikoyatlari to'lqini paydo bo'ldi. Keyinchalik pufakka nisbatan zarba ozgina edi.

Subprime I hajmi jihatidan kichikroq edi - 1990-yillarning o'rtalarida 30 milliard dollarlik ipoteka subprime kreditlash uchun "katta yil" tashkil etdi, 2005 yilga kelib 625 milliard dollarlik ipoteka kreditlari mavjud bo'lib, ularning 507 milliard dollari ipoteka kreditlari bilan ta'minlandi va bu aslida edi "yomon kreditga ega qarz oluvchilar uchun haqiqatan ham yuqori stavkalar". Ipoteka kreditlari asosan belgilangan stavka bo'yicha bo'lib, qarz oluvchilardan daromadlarini hujjatlashtirish orqali to'lashlari mumkinligini isbotlashlari kerak edi.[6] 2006 yilga kelib, boshlang'ich kreditlarning 75 foizi, odatda dastlabki ikki yilga belgilangan, o'zgaruvchan stavkaning bir shaklidir. "[7]

Inqirozga oid ma'lumotlar

2006 yilda, Lehman birodarlar va Bear Stearns Birlashgan ipoteka kreditlarini ishlab chiqarish biznesiga ega bo'lgan doimiy daromadli franchayzalar muvaffaqiyatlarning qochib ketgan voqealari sifatida qaraldi. Ko'pgina sarmoyaviy banklar allaqachon yirik ipoteka stollarini qurishgan va subprime platformalariga katta mablag 'qo'yishgan. AQSh bozori an'anaviy agentlik / CMO modelidan uzoqlashib rivojlangan davrda ipoteka kreditining kelib chiqishi va sekuritizatsiyalash katta daromad keltirdi.[8]

Fanni Mey va Freddi Mak o'zlarining balanslarini sezilarli darajada qisqartirishdi, chunki ipoteka kreditlarining kelib chiqishi hajmlari pasayib ketdi va xususiy yorliqlar sekyuritizatsiyasi 2002 yildan boshlab sezilarli darajada o'sdi.[8] Subprime kreditlash bo'yicha katta miqyosdagi defoltlar 2006 yilda hali bosh sahifaga aylanmagan edi; reyting agentliklari 2006 yil yozida erta signal qo'ng'iroqlarini chalishni boshladilar, ammo yangi kreditlar (2008 yilga kelib) bo'yicha eng katta pul o'tkazmalari kutilgan edi.[8]

Inqiroz bosqichlari

Inqiroz bosqichlarni bosib o'tdi. Birinchidan, 2007 yil oxirida 100 dan ortiq ipoteka kreditlash kompaniyalari bankrot bo'ldi, chunki ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlar endi mablag 'sotib olish uchun investorlarga sotilishi mumkin emas edi. Ikkinchidan, 2007 yil 4-choragidan boshlab va shu vaqtdan boshlab har chorakda moliya institutlari ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlar qiymatini sotib olingan narxlarning bir qismigacha moslashtirganda katta yo'qotishlarni tan oldilar. Uy-joy bozori yomonlashishda davom etayotgan ushbu yo'qotishlar banklarning qarz berish uchun zaif kapital bazasiga ega bo'lishini anglatardi. Uchinchidan, 2008 yil 1-choragida investitsiya banki Bear Stearns operatsiyasini moliyalashtirish uchun qarz olishni davom ettira olmaganidan so'ng, shoshilinch ravishda JP Morgan banki bilan 30 milliard dollarlik davlat kafolati bilan birlashtirildi.[9]

To'rtinchidan, 2008 yil sentyabr oyi davomida tizim buzilishga yaqinlashdi. Sentyabr oyining boshlarida Fanni Mey va Freddi Mak, 5 trillion dollarlik ipoteka majburiyatlarini ifodalovchi, AQSh hukumati tomonidan ipoteka yo'qotishlarining ko'payishi sababli milliylashtirildi. Keyingi, investitsiya banki Lehman birodarlar bankrotlik to'g'risida ariza bergan. Bundan tashqari, AQShning ikkita yirik banki (Washington Mutual va Wachovia) to'lovga qodir bo'lib, kuchliroq banklarga sotildi.[10] Dunyodagi eng yirik sug'urtalovchi, AIG, o'z majburiyatlarini moliyaviy sug'urta deb nomlangan shaklda bajarish qobiliyati bilan bog'liq xavotirlar tufayli AQSh hukumati tomonidan 80% milliylashtirildi kredit svoplari.[11]

Ushbu ketma-ket va muhim institutsional muvaffaqiyatsizliklar, xususan Lehman bankrotligi, kredit bozorlarini egallab olish va global ta'sirni yanada jiddiyroq bo'lishini o'z ichiga oldi. Lehmanning o'zaro bog'liqligi shundan iborat ediki, uning muvaffaqiyatsizligi yirik institutlarning kontragentlar oldidagi majburiyatlarini bajara olish qobiliyatiga nisbatan butun tizimdagi (tizimli) tashvishlarni keltirib chiqardi. Banklarning bir-birlariga hisoblangan foiz stavkalari (qarang TED tarqaldi ) rekord darajaga ko'tarildi va qisqa muddatli mablag'larni olishning turli usullari moliyaviy bo'lmagan korporatsiyalar uchun kamroq imkoniyatga ega bo'ldi.[11]

Aynan shu "kreditning muzlashi", ba'zilari 2008 yil 4-choragida butun dunyo hukumatlari tomonidan amalga oshirilgan katta miqdordagi yordam proseduralarini olib borgan sentyabr oyida kredit bozorlarini deyarli to'liq egallab olish deb ta'riflagan edi. Ushbu nuqtadan oldin AQShning har bir yirik institutsional aralashuvi ijobiy ta'sir ko'rsatgan edi. xok; tanqidchilar bu zarar ko'rgan investor va AQSh hukumatining inqiroz bilan samarali va faol kurashish qobiliyatiga bo'lgan ishonchiga ziyon etkazishdi. Bundan tashqari, AQShning yuqori darajadagi moliyaviy rahbariyatining fikri va ishonchliligi shubha ostiga qo'yildi.[11]

Yaqinda erigan davrdan boshlab inqiroz, ba'zilari chuqur tanazzul deb hisoblagan, boshqalari esa iqtisodiy faoliyatni past darajadagi "qayta tiklash" deb hisoblagan holatga o'tdi, endi bu tizimdan ulkan kredit imkoniyatlari olib tashlandi. AQShning barqaror bo'lmagan qarzlari va iste'mollari inqirozgacha bo'lgan yillarda global iqtisodiy o'sishning muhim omillari bo'ldi. 2009-2011 yillarda AQShda uy-joylarni garovga qo'yishning rekord stavkalari moliya institutlariga zarar etkazishda davom etishi kutilmoqda. Ham uy-joy narxlari, ham qimmatli qog'ozlar bozorining pasayishi tufayli keskin kamaygan boylik AQSh iste'molining inqirozgacha bo'lgan darajaga qaytishiga imkon bermasa kerak.[12]

Tomas Fridman inqiroz qanday bosqichlarni bosib o'tganligini sarhisob qildi:

Bu beparvo ipoteka kreditlari oxir-oqibat portlaganida, bu kredit inqiroziga olib keldi. Banklar kredit berishni to'xtatdilar. Tez orada bu aktsiyalar inqiroziga aylandi, chunki xavotirga tushgan investorlar aktsiyalar portfelini tugatdilar. Kapital inqirozi odamlarni kambag'al his qildi va iste'mol inqiroziga aylandi, shuning uchun avtomobillar, maishiy texnika, elektronika, uy va kiyim-kechak sotib olish jarlikdan qulab tushdi. Bu, o'z navbatida, kompaniyalarning defoltlarini keltirib chiqardi, kredit inqirozini yanada kuchaytirdi va ishsizlik inqiroziga metastaz berdi, chunki kompaniyalar ishchilarni ishdan bo'shatishga shoshilishmoqda.[13]

Alan Greinspan bozorda hozirda uy-joy inventarizatsiyasining rekord darajasi odatiy tarixiy darajaga tushguncha, uy-joy narxlari bo'yicha pastga bosim bo'ladi, deb ta'kidladi. Uy-joy narxlari bo'yicha noaniqliklar saqlanib qolguncha, ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlar qiymati pasayishda davom etadi va banklarning sog'lig'ini xavf ostiga qo'yadi.[14]

Kontekstda ipoteka kreditining inqirozi

Iqtisodchi Nuriel Roubini 2009 yil yanvar oyida yozganidek, ipoteka kreditining past darajadagi defoltlari kengroq ishga tushirildi global kredit inqirozi, ammo bir nechta kredit pufakchalari qulashining bir qismi bo'lgan: "Bu inqiroz nafaqat AQShning uy-joy pufagining yorilishi yoki Qo'shma Shtatlarning ipoteka ipoteka sektorining qulashi oqibati emas. Ushbu falokatni keltirib chiqargan kredit haddan oshishi global edi. Ko'p pufakchalar bor edi Va ular ko'plab mamlakatlarda uy-joy qurishdan tashqari, tijorat ko'chmas mulki uchun ipoteka va kreditlar, kredit kartalar, avtoulov kreditlari va talabalar kreditlariga qadar kengaytirildi.[15]

Ushbu kreditlar va ipoteka kreditlarini murakkab, toksik va halokatli moliyaviy vositalarga aylantirgan qimmatli qog'ozlar uchun pufaklar mavjud edi. Hali ham mahalliy hukumatning qarz olishlari, kaldıraçlı sotib olish, to'siq mablag'lari, tijorat va sanoat kreditlari, korporativ obligatsiyalar, tovar va ssop svoplari uchun ko'proq pufaklar bor edi. "Bu ko'plab pufakchalarning yorilishi, bu inqirozga sabab bo'lmoqda global miqyosda tarqaladi va uning ta'sirini oshiradi.[15]

Fed raisi Ben Bernanke 2009 yil yanvaridagi chiqish paytida inqirozni quyidagicha umumlashtirdi:

"Deyarli bir yarim yildan beri global moliya tizimi favqulodda stressni boshdan kechirmoqda - bu hozirgi paytda global iqtisodiyotga hal qiluvchi ta'sirni yanada kengroq qamrab olgan. Inqirozning taxminiy sababi Qo'shma Shtatlardagi uy-joy tsiklining o'zgarishi edi ipoteka kreditlari bo'yicha huquqbuzarliklarning ko'payishi va ko'plab moliyaviy tashkilotlarga katta zarar etkazgan va investorlarning kredit bozorlariga bo'lgan ishonchini silkitgan. Ammo, garchi subprime inqirozi inqirozni keltirib chiqargan bo'lsa-da, AQSh ipoteka bozoridagi o'zgarishlar juda ko'p jihatlarning bittasi edi. kreditlar portlashi yanada kattaroq va qamrab oladigan bo'lib, ularning ta'siri ipoteka bozoridan boshqa ko'plab kredit turlariga ta'sir ko'rsatdi.Bu kengroq kredit portlashi jihatlariga anderrayting standartlarining keng pasayishi, investorlar va reyting agentliklari tomonidan kredit nazorati buzilishi, murakkab va shaffof bo'lmagan kreditlarga bo'lgan ishonchning kuchayishi kiradi. stress ostida mo'rt bo'lgan asboblar va tavakkal qilish uchun juda kam kompensatsiya ing. Kredit boomining to'satdan tugashi keng moliyaviy va iqtisodiy ta'sirga ega bo'ldi. Moliya institutlari o'zlarining kapitalini zararlar va ishdan bo'shatishlar natijasida tugatgan va ularning balanslari murakkab kredit mahsulotlari va noaniq qiymatga ega bo'lgan boshqa likvidli aktivlar tomonidan tiqilib qolgan. Borayotgan kredit tavakkalchiliklari va tavakkalchilikdan qattiq qochish kredit tarqalishini misli ko'rilmagan darajaga olib keldi va sekuritizatsiyalangan aktivlar bozorlari, hukumat kafolati bo'lgan ipoteka qimmatli qog'ozlaridan tashqari. Kuchaygan tizimli xatarlar, aktivlar qiymatining pasayishi va kreditning kuchayishi o'z navbatida biznesga va iste'molchilar ishonchiga katta zarar etkazdi va global iqtisodiy faoliyatning keskin pasayishiga olib keldi. Yo'qotilgan mahsulot, yo'qolgan ish joylari va boylik nuqtai nazaridan zarar allaqachon sezilarli. "[16]

Tomas Fridman 2008 yil noyabridagi inqiroz sabablarini umumlashtirdi:

Hukumatlar bu deflyatsion pasayish spiralini ushlashda muammoga duch kelmoqdalar - ehtimol bu moliyaviy inqiroz biz ilgari hech qachon ko'rmagan to'rtta kimyoviy moddalarni birlashtirganligi sababli va ularning o'zaro ta'sirlari qanchalik zarar ko'rganligini va hali ham bo'lishi mumkinligini tushunmayapmiz. Ushbu kimyoviy moddalar: 1) ulkan kaldıraç - har bir 1 dollar uchun 30 dollar tikkan mablag'larni to'sish uchun uylarni hech narsaga sotib olmagan xaridorlarning har biri tomonidan naqd pulda; 2) odamlar tushunganidan ko'ra bir-biriga chambarchas bog'liq bo'lgan jahon iqtisodiyoti, bunga bugungi kunda moliyaviy jihatdan qiyin bo'lgan Britaniya politsiya bo'limlari misol bo'la oladi, chunki ular o'zlarining jamg'armalarini Islandiyaning onlayn banklariga joylashtirmoqdalar - biroz yaxshiroq hosil olish uchun - bu ishdan chiqqan; 3) global miqyosda bir-biriga chambarchas bog'liq moliyaviy vositalar, ular bilan CE.O.ning muomalasining aksariyati ular qanday ishlashini tushunmagan va tushunmaydilar - ayniqsa salbiy tomoni; 4) Amerikada bizning toksik ipoteka kreditlarimiz bilan boshlangan moliyaviy inqiroz. Meksika yoki Tailandda inqiroz boshlanganda, biz o'zimizni himoya qila olamiz; Amerikada boshlanganda, hech kim qila olmaydi. Siz shuncha kaldıraçla shu qadar murakkablik bilan global miqyosdagi integratsiyani birlashtirdingiz va Amerikadagi inqirozni boshladingiz va sizda juda portlovchi holat mavjud.[17]

Subprime bozor ma'lumotlari

AQSh subpoteka kreditlari qiymati 2007 yil mart holatiga ko'ra 1,3 trln.[18] 7,5 milliondan ortiq birinchigarovga olish ipoteka kreditlari.[19] 2007 yil oktyabr oyi holatiga ko'ra ipoteka kreditlari (ARM) bilan tartibga solinadigan submpime kreditlarining taxminan 16% 90 kunlik muddati o'tgan yoki qarzni undirish to'g'risidagi protseduralarda 2007 yil oktyabr oyiga kelib, 2005 yilga nisbatan qariyb uch baravar ko'p bo'lgan.[20] 2008 yil yanvarga kelib, huquqbuzarlik darajasi 21% ga ko'tarildi[21] va 2008 yil may oyiga qadar bu 25% ni tashkil etdi.[22]

2004 yildan 2006 yilgacha bo'lgan davrda ipoteka kreditlarining ulushi umumiy kelib chiqishga nisbatan 18% -21% gacha bo'lgan, 2001-2003 yillarda va 2007 yilda 10% dan kam bo'lgan.[23][24] Subprime ARMlar AQShda berilgan qarzlarning faqat 6,8 foizini tashkil etadi, ammo ular 2007 yilning uchinchi choragida boshlangan qarzdorlikning 43 foizini tashkil etadi.[25] 2007 yil davomida qariyb 1,3 million ko'chmas mulk 2,2 millionga mol-mulkni garovga qo'yishga majbur bo'ldi, bu 2006 yildagiga nisbatan 79 foizga va 75 foizga ko'pdir. Ilovani garovga qo'yish to'g'risidagi arizalar, shu jumladan sukut bo'yicha ogohlantirishlar, kim oshdi savdosi to'g'risidagi bildirishnomalar va bankni qaytarib olish bir xil mulk to'g'risida bir nechta xabarnomalarni o'z ichiga olishi mumkin.[26]

2008 yil davomida bu 2,3 millionga etdi, bu 2007 yilga nisbatan 81 foizga ko'pdir.[27] 2007 yil avgust va 2008 yil sentyabr oylari oralig'ida uy egalarining qarz beruvchilari tomonidan 851,000 ta uylar qaytarib olingan.[28] Hibsga olish, ma'lum shtatlarda, garovga qo'yilgan hujjatlar soni va stavkasi bo'yicha jamlangan.[29] O'nta shtat 2008 yildagi qarzdorlik to'g'risidagi arizalarning 74 foizini tashkil etdi; eng yaxshi ikkitasi (Kaliforniya va Florida) 41% ni tashkil etdi. To'qqizta shtat o'rtacha qarzdorlik ko'rsatkichidan 1,84 foiz uy xo'jaliklaridan yuqori bo'lgan.[30]

Ipoteka bozorining bahosi 12 trln[31] 2008 yil avgust holatiga ko'ra qarzlarning qariyb 6,41 foizi va qarzdorlik qarzdorligining 2,75 foizi.[32] Yuqori foiz stavkalari bo'yicha qayta tiklanadigan subprime stavkasi bo'yicha ipoteka kreditlarining (ARM) taxminiy qiymati 2007 yil uchun 400 milliard AQSh dollarini va 2008 yil uchun 500 milliard dollarni tashkil etadi. Qayta tiklash faolligi pasayishidan oldin 2008 yil mart oyida 100 milliard dollarga teng bo'lgan oylik eng yuqori darajaga ko'tarilishi kutilmoqda.[33] O'rtacha 450,000 subprime ARM har chorakda birinchi stavkaning ko'tarilishini 2008 yilda rejalashtirilgan.[34]

Taxminan 8,8 million xonadon egalari (umumiy qariyb 10,8%) 2008 yil mart holatiga ko'ra nolga teng yoki manfiy kapitalga ega, ya'ni ularning uylari ipotekadan pastroq qiymatga ega. Bu kredit reytingi ta'siriga qaramay, uydan "yurish" uchun rag'bat beradi.[35]

2008 yil yanvariga kelib, sotilmagan yangi uylarning ro'yxati 2007 yil dekabr oyidagi savdo hajmi bo'yicha 9,8 oyni tashkil etdi, bu 1981 yildan beri eng yuqori ko'rsatkichdir.[36] Bundan tashqari, sotilmagan to'rt millionga yaqin mavjud bo'lgan uylarning sotuvga qo'yilishi,[37] shu jumladan bo'sh bo'lgan 2,9 millionga yaqin.[38] Uy-ro'zg'or buyumlarining bu ortiqcha zaxirasi narxlarga sezilarli darajada pastga bosim o'tkazmoqda. Narxlarning pasayishi bilan ko'proq uy egalari to'lovni to'lamaslik va garovga qo'yilish xavfi ostida. S & P / Case-Shiller narxlari indeksiga ko'ra, 2007 yil noyabr oyiga qadar AQShdagi uy-joylarning o'rtacha narxi 2006 yil 2-choragidan taxminan 8 foizga pasaygan.[39] va 2008 yil may oyiga kelib ular 18,4% ga kamaydi.[40] 2007 yil dekabrida narxlarning pasayishi o'tgan yilga nisbatan 10,4%, 2008 yil may oyida esa 15,8% ni tashkil etdi.[41] Uy-joy narxlari pasayishi davom etishi kutilmoqda, bu ortiqcha uylar (ortiqcha ta'minot) inventarizatsiyasi odatdagi darajalarga tushguncha.

Uy xo'jaliklarining qarzdorlik statistikasi

1981 yilda AQShning xususiy qarzi 123 foizni tashkil etdi yalpi ichki mahsulot (iqtisodiyot hajmi o'lchovi); 2008 yilning uchinchi choragida bu 290 foizni tashkil etdi. 1981 yilda, uy qarzi YaIMning 48 foizini tashkil etdi; 2007 yilda bu 100 foizni tashkil etdi.[42]

Uy-joy narxi oshib borar ekan, iste'molchilar kamroq tejashdi[43] ham qarz olish, ham ko'proq sarflash. Iste'molchilik madaniyati "zudlik bilan qondirishga asoslangan iqtisodiyot" omilidir.[44] 2005 yildan boshlab Amerika uy xo'jaliklari o'zlarining 99,5 foizidan ko'prog'ini sarfladilar bir martalik shaxsiy daromad iste'mol yoki foiz to'lovlari bo'yicha.[45] Agar bu hisob-kitoblardan asosan mulkdorlar tomonidan egalik qilinadigan uy-joylarga tegishli hisob-kitoblar olib tashlansa, amerikalik uy xo'jaliklari 1999 yildan boshlab har yili shaxsiy daromadlaridan ko'proq mablag 'sarfladilar.[46]

Uy xo'jaliklarining qarzi 1974 yil oxiriga kelib 705 milliard dollardan o'sdi, bu 60% bir martalik shaxsiy daromad, 2000 yil oxirida 7,4 trillion dollarga, nihoyat 2008 yil o'rtalarida 14,5 trillion dollarga, shaxsiy daromadlarning 134%.[47] 2008 yil davomida AQShning odatdagi uy xo'jaliklari 13 ta kredit kartalariga egalik qildilar, ularning 40% uy balansi 1970 yildagi 6% ga teng edi.[48] Yalpi ichki mahsulotga nisbatan AQShning uy-joy ipoteka qarzi 1990-yillar davomida o'rtacha 46% dan 2008 yilda 73% gacha o'sdi va 10,5 trln.[49]

Moliyaviy sektor qarzdorlik statistikasi

Martin Wolf "AQShda moliya sektorining holati Yaponiyadagiga qaraganda ancha muhimroq bo'lishi mumkin. AQShning katta miqdordagi qarzdorligi nodavlat korporatsiyalar tomonidan emas, balki uy xo'jaliklari va moliya sektoriga tegishli edi. moliya sektori 1981 yildagi YaIMning 22 foizidan 2008 yilning uchinchi choragida 117 foizgacha o'sdi, moliyaviy bo'lmagan korporatsiyalarning qarzi esa YaIMning 53 foizidan 76 foizigacha ko'tarildi. Shunday qilib, moliya institutlarining xohishi balanslarni qisqartirish AQShda turg'unlikning yanada katta sababi bo'lishi mumkin. "[42]

Kredit xavfi

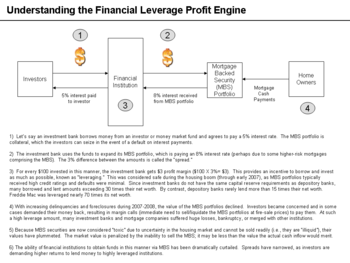

An'anaga ko'ra, kreditorlar (asosan ular bo'lgan) tejamkorlik ) ular bergan ipoteka kreditlari bo'yicha kredit xavfini o'z zimmasiga oldi. So'nggi 60 yil ichida turli xil moliyaviy yangiliklar deb nomlangan jarayon orqali qarz beruvchilarga ipoteka kreditlari bo'yicha to'lovlarni olish huquqini sotish imkoni boricha asta-sekinlik bilan erishildi. sekuritizatsiya. Natijada paydo bo'lgan qimmatli qog'ozlar deyiladi ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlar (MBS) va garovga qo'yilgan qarz majburiyatlari (CDO). Aksariyat amerikalik ipoteka ipoteka hovuzlari tomonidan amalga oshiriladi, bu MBS va CDOlarning umumiy muddati. 2008 yil o'rtalarida 10,6 trillion AQSh dollari miqdoridagi uy-joy ipotekasining 6,6 trillion dollari ipoteka havzalarida, 3,4 trillion dollari an'anaviy depozit tashkilotlarida saqlandi.[50]Ushbu "tarqatish uchun kelib chiqqan" model shuni anglatadiki, MBS va CDO-larga ega bo'lgan investorlar ham bir necha turdagi xatarlarga ega va bu turli xil oqibatlarga olib keladi. Umuman olganda, xavfning beshta asosiy turi mavjud:[51][52]

21-asrning boshlarida ushbu yangiliklar ipoteka kreditlari uchun "tarqatish uchun kelib chiqish" modelini yaratdi, ya'ni ipoteka qarzlar singari deyarli qimmatli qog'ozlarga aylandi. Subprime kreditlari qaytarilish xavfi yuqori bo'lganligi sababli, tejamkorlik tashkilotlari yoki tijorat banklari tomonidan katta miqdordagi subpime kreditlarining kelib chiqishi sekuritizatsiyasiz amalga oshirilmadi.

Tizimli nuqtai nazardan, sekuritizatsiyaning ustunligi ipoteka bozoridagi xatarlarni boshqa qimmatli qog'ozlar bozorlari, xususan tartibga solinmagan qimmatli qog'ozlar bozorlari xatarlariga o'xshash holga keltirdi. Umuman olganda, ushbu bozorlarda tavakkalchilikning beshta asosiy turi mavjud:[51][52][53]

| Ism | Tavsif |

|---|---|

| Kredit xavfi | qarz oluvchining to'lovlarni to'lamasligi va / yoki kreditning ta'minoti ta'minot qiymatini yo'qotish xavfi. |

| Aktiv narxlari xavfi | aktivning o'zi (bu holda MBS yoki asosiy ipoteka) qiymati pasayib, moliyaviy yo'qotishlarga olib keladigan xavf, pastga tushirish va ehtimol margin qo'ng'iroqlari |

| Qarshi tomon xavf | qarz oluvchidan tashqari MBS yoki lotin shartnomasi tomoni o'z majburiyatlarini bajara olmasligi yoki bajarishni istamasligi xavfi. |

| Tizimli xavf | Ushbu va boshqa xavf-xatarlarning umumiy ta'siri yaqinda chaqirildi tizimli xavf bu butun moliyaviy tizimda keskin "sezgir" yoki jiddiy o'zgarishlarni anglatadi, bu juda "o'zaro bog'liq" xatti-harakatlarni keltirib chiqaradi va ushbu tizimga zarar etkazishi mumkin. |

| Likvidlik xavfi | Institutsional darajada, bu tizimdagi pulning tez qurishi va xo'jalik yurituvchi sub'ekt g'ayrioddiy yo'qotishlarni oldini olish uchun tez orada o'z faoliyatini moliyalashtirish uchun naqd pul ololmasligi xavfi. |

Bu shuni anglatadiki, ipoteka bozorida qarz oluvchilar endi kredit xatarlari keskin ko'tarilishidan oldin defoltni to'lashlari va pul oqimlarini juda sezilarli darajada kamaytirishlari shart. Moddiy yoki taxmin qilinadigan xavfga ta'sir qiluvchi har qanday omillar - ko'chmas mulk narxining pasayishi yoki yirik kontragentning bankrotligi - bu tashkilotlarning tizimli xavfi va likvidliligi xavfining ko'tarilishiga olib kelishi va butun ipoteka sanoatiga salbiy ta'sir ko'rsatishi mumkin. Xavf so'nggi yillarda yuzaga kelganidek, uy xo'jaliklari va korxonalar o'rtasida yuqori qarz darajasi (moliyaviy ta'sir kuchi) bilan kattalashishi mumkin. Va nihoyat, Amerika ipoteka krediti bilan bog'liq xatarlar global ta'sirga ega, chunki MBS bozori ulkan, global, moliyaviy bozor hisoblanadi.

Ning juda yangi yangiliklari alohida tashvishga solmoqda kredit svoplari (CDS). MBS-ga sarmoyadorlar CDS sotib olish orqali kredit xavfidan sug'urta qilishlari mumkin, ammo xavf oshgani sayin, CDS shartnomalaridagi kontragentlar garovni etkazib berishlari va ko'proq to'lovlar zarur bo'lganda zaxiralarni yaratishi kerak. Subprime bozorida xavfning ko'tarilish tezligi va jiddiyligi tizimda noaniqlikni keltirib chiqardi, investorlar AIG singari ulkan CDS kontragentlari o'z majburiyatlarini bajara olmasliklari mumkinmi deb hayron bo'lishdi.

Subprime inqiroziga olib keladigan xavf turlarini tushunish

Ushbu inqirozning sabablari har xil va murakkab.[54] Jahon iqtisodiyoti orqali to'lqin ta'sirini tushunish va boshqarish hukumatlar, korxonalar va investorlar uchun juda muhim muammolarni keltirib chiqaradi. Inqirozni bir qator omillarga, masalan, uy egalarining bunga qodir emasligi bilan bog'lash mumkin ipoteka to'lovlar; qarz oluvchi va / yoki qarz beruvchining yomon qarori; keyinchalik ipoteka imtiyozlari, masalan, "teaser" foiz stavkalari keyinchalik sezilarli darajada ko'tariladi.

Bundan tashqari, uy-joy narxlarining pasayishiga olib keldi qayta moliyalashtirish qiyinroq. Natijada moliyaviylashtirish va yangiliklar sekuritizatsiya, uy-joy mulkdorlari tomonidan ipoteka to'lovlarini bajara olmaslik bilan bog'liq xatarlar bir qator oqibatlarga olib keladigan tarzda keng taqsimlandi. Xavfning beshta asosiy toifasi mavjud:

- Kredit xavfi: An'anaga ko'ra, qarzni to'lash xavfi (deyiladi) kredit xavfi ) kreditni keltirgan bank tomonidan qabul qilinadi. Biroq, sekuritizatsiyadagi yangiliklar tufayli kredit xavfi ko'pincha uchinchi tomon investorlariga o'tkaziladi. Ipoteka to'lovlariga bo'lgan huquqlar turli xil murakkab investitsiya vositalarida qayta paketlangan bo'lib, odatda quyidagicha tasniflangan ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlar (MBS) yoki garovga qo'yilgan qarz majburiyatlari (CDO). CDO, aslida, mavjud qarzni qayta to'ldirishdir va so'nggi yillarda MBS garovi emissiyaning katta qismini tashkil etdi. MBS yoki CDO sotib olish va kredit xavfini o'z zimmasiga olish evaziga uchinchi tomon investorlari ipoteka aktivlari va tegishli pul oqimlari bo'yicha da'vo olishadi, bu esa defolt holatida garovga aylanadi. Defoltlardan himoya qilishning yana bir usuli bu kreditni almashtirish, unda bir tomon mukofot puli to'laydi, ikkinchisi esa ma'lum bir moliyaviy vosita buzilgan taqdirda ularni to'laydi.

- Aktiv narxining xavfi: MBS va CDO aktivlarini baholash murakkab va bog'liqdir "adolatli qiymat "yoki"bozorga belgi "buxgalteriya hisobi keng talqin qilinishi kerak. Baholash subpoteka ipoteka to'lovlarining yig'ish qobiliyatidan va ushbu aktivlarni sotish mumkin bo'lgan hayotiy bozor mavjudligidan kelib chiqadi, ular o'zaro bog'liqdir. Ipoteka kreditlarining ko'tarilish darajasi, bunday aktivlarga bo'lgan talabni pasaytirdi. Banklar va institutsional investorlar o'zlarining MBS qiymatini pastga qarab qayta baholaganlarida katta zararlarni tan oldilar .. MBS yoki CDO aktivlaridan foydalangan holda qarz olgan bir nechta kompaniyalar. garov duch kelgan margin qo'ng'iroqlari, chunki qarz beruvchilar pullarini qaytarib olish uchun o'zlarining shartnoma huquqlarini amalga oshirdilar.[55] Odil qiymatni hisobga olish to'xtatib turilishi yoki vaqtincha o'zgartirilishi kerakligi to'g'risida bir muncha munozaralar mavjud, chunki qiymati qiyin bo'lgan MBS va CDO aktivlarining katta hajmdagi hisobdan chiqarilishi inqirozni yanada kuchaytirishi mumkin.[56]

- Likvidlik xavfi: Ko'pgina kompaniyalar naqd pul ishlash uchun (ya'ni likvidlik) qisqa muddatli moliyalashtirish bozorlariga kirishga ishonadilar, masalan tijorat qog'ozi va bozorlarni qayta sotib olish. Kompaniyalar va tarkibiy investitsiya vositalari (SIV) ko'pincha tijorat qog'ozi berish, garov sifatida ipoteka aktivlarini yoki CDO-ni garovga qo'yish orqali qisqa muddatli kreditlar olishadi. Investorlar tijorat qog'ozi evaziga naqd pul bilan ta'minlaydilar, pul bozoridagi foizlarni olishadi. Biroq, ipoteka aktivlari garovining subprime va Alt-A kreditlari bilan bog'liqligi bilan bog'liq xavotirlar tufayli ko'plab kompaniyalarning bunday qog'ozni chiqarish qobiliyatiga sezilarli ta'sir ko'rsatildi.[57] 2007 yil 18 oktyabr holatiga chiqarilgan tijorat qog'ozi hajmi 8 avgust darajasidan 25 foizga, 888 milliard dollarga kamaydi. Bundan tashqari, sarmoyadorlar tomonidan tijorat qog'ozi uchun kredit berish uchun olinadigan foiz stavkasi tarixiy darajadan sezilarli darajada oshdi.[58]

- Kontragent tavakkalchiligi: yirik investitsiya banklari va boshqa moliya institutlari muhim pozitsiyalarni egallashdi kredit lotin bitimlar, ularning ba'zilari kreditni to'lashni sug'urtalash shakli bo'lib xizmat qiladi. Yuqoridagi xatarlar ta'siri tufayli investitsiya banklarining moliyaviy holati pasayib, ular uchun xavfni oshirishi mumkin kontragentlar va moliyaviy bozorlarda yanada noaniqliklar yaratish. Yo'q qilish va qutqarish Bear Stearns qisman ushbu hosilalardagi roli bilan bog'liq edi.[59]

- Tizimli xavf: yaqinda ushbu va boshqa xatarlarning umumiy ta'siri chaqirildi tizimli xavf. Nobel mukofoti sovrindori Dr. A. Maykl Spens, "ilgari o'zaro bog'liq bo'lmagan xatarlar o'zgarganda va juda o'zaro bog'liqlikda moliyaviy tizimda tizimli xavf kuchayadi. Bu sodir bo'lganda sug'urta va diversifikatsiya modellari muvaffaqiyatsizlikka uchraydi. Hozirgi inqiroz va uning kelib chiqishining ikkita diqqatga sazovor tomoni bor. Ulardan biri tizimli xavf barqaror ravishda qurilgan Ikkinchidan, ushbu birikma beparvo bo'lib qoldi yoki unga e'tibor berilmadi. Bu shuni anglatadiki, u kechikmaguncha aksariyat ishtirokchilar tomonidan sezilmadi. Xavfni qayta taqsimlash va kamaytirishga mo'ljallangan moliyaviy yangilik asosan paydo bo'ladi Oldinda turgan muhim muammo - bu dinamikani moliyaviy beqarorlikka nisbatan erta ogohlantirish tizimining analitik asosi sifatida yaxshiroq tushunishdir. "[60]

Korporatsiyalar va investorlarga ta'siri

O'rtacha sarmoyadorlar va korporatsiyalar ipoteka egalarining to'lovni amalga oshira olmasligi sababli turli xil xavf-xatarlarga duch kelishmoqda. Ular yuridik shaxsga qarab farq qiladi. Tashkilot turlari bo'yicha ba'zi umumiy ta'sirlarga quyidagilar kiradi:

- Tijorat / depozitar bank korporatsiyalari: yirik banklar tomonidan e'lon qilingan daromadlarga aktivlarning har xil turlari, jumladan, ipoteka kreditlari, kredit kartalar va avtokreditlar uchun berilgan ssudalar salbiy ta'sir ko'rsatmoqda. Kompaniyalar ushbu aktivlarni (debitorlik qarzlarini) yig'imlarni baholash asosida baholashadi. Ushbu baholashni to'g'rilash uchun kompaniyalar joriy davrdagi xarajatlarni qayd etib, ularning yomon qarz zaxiralarini ko'paytiradilar va daromadlarni kamaytiradilar. Aktivlarni baholashdagi tez yoki kutilmagan o'zgarishlar foyda va aktsiyalar bahosidagi o'zgaruvchanlikka olib kelishi mumkin. Kreditorlarning kelajakdagi kollektsiyalarni bashorat qilish qobiliyati o'zgaruvchanligi ko'pligiga bog'liq bo'lgan murakkab vazifadir.[61] Bundan tashqari, bankning ipoteka kreditidan mahrum bo'lganligi, agar zarur bo'lsa, kapital zaxiralarining me'yoriy talablariga muvofiqligini ta'minlash uchun kredit berishni kamaytirishi yoki kapital bozorlaridan qo'shimcha mablag 'qidirishi mumkin. Ko'pgina banklar, shuningdek, ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlarni sotib oldilar va ushbu investitsiyalardan zarar ko'rdilar.

- Investitsiya banklari, ipoteka kreditorlari va ko'chmas mulk investitsiyalari trestlari: Ushbu sub'ektlar banklar uchun shunga o'xshash xatarlarga duch kelmoqdalar, ammo mijozlarning bank depozitlari bilan ta'minlangan barqarorlikka ega emaslar. Ular CDO orqali muntazam ravishda yangi moliyalashtirishni ta'minlash qobiliyatiga sezilarli darajada ishonadigan biznes modellariga ega tijorat qog'ozi emissiya, past foizli stavkalar bilan qisqa muddatli qarz olish va yuqori foizli stavkalar bilan uzoqroq muddatli kreditlar berish (ya'ni foiz stavkasidan foyda olish "tarqalish".) Bunday firmalar ko'proq foyda keltirar edilar. kaldıraçlı uy-joy qiymatining oshishi bilan ular (ya'ni, qancha ko'p qarz olishgan va qarz berishgan) bo'lishdi. For example, investment banks were leveraged around 30 times equity, while commercial banks have regulatory leverage caps around 15 times equity. In other words, for each $1 provided by investors, investment banks would borrow and lend $30.[62] However, due to the decline in home values, the mortgage-backed assets many purchased with borrowed funds declined in value. Further, short-term financing became more expensive or unavailable. Such firms are at increased risk of significant reductions in book value owing to asset sales at unfavorable prices and many have filed bankruptcy or been taken over.[63]

- Insurance companies: Corporations such as AIG provide insurance products called kredit svoplari, which are intended to protect against credit defaults, in exchange for a premium or fee. They are required to post a certain amount of collateral (e.g., cash or other liquid assets) to be in a position to provide payments in the event of defaults. The amount of capital is based on the credit rating of the insurer. Due to uncertainty regarding the financial position of the insurance company and potential risk of default events, credit agencies may downgrade the insurer, which requires an immediate increase in the amount of collateral posted. This risk-downgrade-post cycle can be circular and destructive across multiple firms and was a factor in the AIG bailout. Further, many major banks insured their mortgage-backed assets with AIG. Had AIG been allowed to go bankrupt and not pay these banks what it owed them, these institutions could have failed, causing risk to the entire financial system. Since September 2008, the U.S. government has since stepped in with $150 billion in financial support for AIG, much of which flows through AIG to the banks.[64][65]

- Special purpose entities (SPE): These are legal entities often created as part of the securitization process, to essentially remove certain assets and liabilities from bank balance sheets, theoretically insulating the parent company from credit risk. Like corporations, SPE are required to revalue their mortgage assets based on estimates of collection of mortgage payments. If this valuation falls below a certain level, or if cash flow falls below contractual levels, investors may have immediate rights to the mortgage asset collateral. This can also cause the rapid sale of assets at unfavorable prices. Other SPE called structured investment vehicles (SIV) issue commercial paper and use the proceeds to purchase securitized assets such as CDO. These entities have been affected by mortgage asset devaluation. Several major SIV are associated with large banks. SIV legal structures allowed financial institutions to remove large amounts of debt from their balance sheets, enabling them to use higher levels of leverage and increasing profitability during the boom period. As the value of the SIV assets was reduced, the banks were forced to bring the debt back onto their books, causing an immediate need for capital (to achieve regulatory minimums) thereby aggravating liquidity challenges in the banking system.[66] Some argue this shifting of assets off-balance sheet reduces financial statement transparency; SPE came under scrutiny as part of the Enron debacle, shuningdek. Financing through off-balance sheet structures is thinly regulated. SIV and similar structures are sometimes referred to as the soya bank tizimi.[67]

- Investors: Stocks or obligatsiyalar of the entities above are affected by the lower earnings and uncertainty regarding the valuation of mortgage assets and related payment collection. Many investors and corporations purchased MBS or CDO as investments and incurred related losses.

Understanding financial institution solvency

Critics have argued that due to the combination of high leverage and losses, the U.S. banking system is effectively to'lovga layoqatsiz (i.e., equity is negative or will be as the crisis progresses),[68] while the banks counter that they have the cash required to continue operating or are "well-capitalized." As the crisis progressed into mid-2008, it became apparent that growing losses on ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlar at large, systemically-important institutions were reducing the total value of assets held by particular firms to a critical point roughly equal to the value of their liabilities.

A bit of accounting theory is helpful to understanding this debate. It is an accounting shaxsiyat (i.e., an equality that must hold true by definition) that aktivlar equals the sum of majburiyatlar va tenglik. Equity consisted primarily of the umumiy yoki imtiyozli aktsiya va ajratilmagan daromad of the company and is also referred to as poytaxt. The moliyaviy hisobot that reflects these amounts is called the balanslar varaqasi.

If a firm is forced into a negative equity scenario, it is technically insolvent from a balance sheet perspective. However, the firm may have sufficient cash to pay its short-term obligations and continue operating. Bankrotlik occurs when a firm is unable to pay its immediate obligations and seeks legal protection to enable it to either re-negotiate its arrangements with creditors or liquidate its assets. Pertinent forms of the accounting equation for this discussion are shown below:

- Assets = Liabilities + Equity

- Equity = Assets - Liabilities = Net worth or capital

- Financial leverage ratio = Assets / Equity

If assets equal liabilities, then equity must be zero. While asset values on the balance sheet are marked down to reflect expected losses, these institutions still owe the kreditorlar the full amount of liabilities. To use a simplistic example, Company X used a $10 equity or capital base to borrow another $290 and invest the $300 amount in various assets, which have fallen 10% in value to $270. This firm was "leveraged" 30:1 ($300 assets / $10 equity = 30) and now has assets worth $270, liabilities of $290 and equity of salbiy $20. Such leverage ratios were typical of the larger investment banks during 2007. At 30:1 leverage, it only takes a 3.33% loss to reduce equity to zero.

Banks use various regulatory measures to describe their financial strength, such as 1-darajali kapital. Such measures typically start with equity and then add or subtract other measures. Banks and regulators have been criticized for including relatively "weaker" or less tangible amounts in regulatory capital measures. For example, deferred tax assets (which represent future tax savings if a company makes a profit) and intangible assets (e.g., non-cash amounts like goodwill or trademarks) have been included in tier 1 capital calculations by some financial institutions. In other cases, banks were legally able to move liabilities off their balance sheets via structured investment vehicles, which improved their ratios. Critics suggest using the "tangible common equity" measure, which removes non-cash assets from these measures. Generally, the ratio of tangible common equity to assets is lower (i.e., more conservative) than the tier 1 ratio.[69]

Banks and governments have taken significant steps to improve capital ratios, by issuing new preferred stock to private investors or to the government via bailouts, and cutting dividends.

Understanding the events of September 2008

Liquidity risk and the money market funding engine

During September 2008, money market mutual funds began to experience significant withdrawals of funds by investors in the wake of the Lehman birodarlar bankruptcy and AIG bailout. This created a significant risk because money market funds are integral to the ongoing financing of corporations of all types. Individual investors lend money to money market funds, which then provide the funds to corporations in exchange for corporate short-term securities called asset-backed commercial paper (ABCP).[70]

However, a potential bank boshqaruvi had begun on certain money market funds. If this situation had worsened, the ability of major corporations to secure needed short-term financing through ABCP issuance would have been significantly affected. To assist with liquidity throughout the system, the Treasury and Federal Reserve Bank announced that banks could obtain funds via the Federal Reserve's Discount Window using ABCP as collateral.[70]

Pul bozoridagi o'zaro fondlar potentsialini to'xtatish uchun G'aznachilik 19 sentyabr kuni investitsiyalarni sug'urtalash bo'yicha 50 mlrd dollarlik yangi dasturni e'lon qildi. Federal depozitlarni sug'urtalash korporatsiyasi (FDIC) program for regular bank accounts.[71]

Key risk indicators

Key risk indicators became highly volatile during September 2008, a factor leading the U.S. government to pass the 2008 yilgi favqulodda iqtisodiy barqarorlashtirish to'g'risidagi qonun. "TED tarqaldi ” is a measure of credit risk for inter-bank lending. It is the difference between: 1) the risk-free three-month U.S. treasury bill (t-bill) rate; and 2) the three-month London Interbank Borrowing Rate (LIBOR), which represents the rate at which banks typically lend to each other. A higher spread indicates banks perceive each other as riskier counterparties. The t-bill is considered "risk-free" because the full faith and credit of the U.S. government is behind it; theoretically, the government could just print money so investors get their money back at the maturity date of the t-bill.

The TED Spread reached record levels in late September 2008. The diagram indicates that the Treasury yield movement was a more significant driver than the changes in LIBOR. A three-month t-bill yield so close to zero means that people are willing to forego interest just to keep their money (principal) safe for three months—a very high level of risk aversion and indicative of tight lending conditions. Driving this change were investors shifting funds from money market funds (generally considered nearly risk free but paying a slightly higher rate of return than t-bills) and other investment types to t-bills.[72]

In addition, an increase in LIBOR means that financial instruments with variable interest terms are increasingly expensive. For example, adjustable rate mortgages, car loans and credit card interest rates are often tied to LIBOR; some estimate as much as $150 trillion in loans and hosilalar are tied to LIBOR.[73] Higher interest rates place additional downward pressure on consumption, increasing the risk of recession.

Credit default swaps and the subprime mortgage crisis

Credit defaults swaps (CDS) are insurance contracts, typically used to protect bondholders from the risk of default, called kredit xavfi. As the financial health of banks and other institutions deteriorated due to losses related to mortgages, the likelihood that those providing the insurance would have to pay their counterparties increased. This created uncertainty across the system, as investors wondered which companies would be forced to pay to cover defaults.

For example, Company Alpha issues bonds to the public in exchange for funds. The bondholders pay a financial institution an insurance premium in exchange for it assuming the credit risk. If Company Alpha goes bankrupt and is unable to pay interest or principal back to its bondholders, the insurance company would pay the bondholders to cover some or all of the losses. In effect, the bondholder has "swapped" its credit risk with the insurer. CDS may be used to insure a particular financial exposure as described in the example above, or may be used speculatively. Because CDS may be traded on public exchanges like stocks, or may be privately negotiated, the exact amount of CDS contracts outstanding at a given time is difficult to measure. Trading of CDS increased 100-fold from 1998 to 2008. Estimates for the face value of debt covered by CDS contracts range from U.S. $33 to $47 trillion as of November 2008.[74]

Many CDS cover ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlar yoki garovga qo'yilgan qarz majburiyatlari (CDO) involved in the subprime mortgage crisis. CDS are lightly regulated. There is no central clearinghouse to honor CDS in the event a key player in the industry is unable to perform its obligations. Required corporate disclosure of CDS-related obligations has been criticized as inadequate. Insurance companies such as AIG, MBIA, and Ambac faced ratings downgrades due to their potential exposure due to widespread debt defaults. These institutions were forced to obtain additional funds (capital) to offset this exposure. In the case of AIG, its nearly $440 billion of CDS linked to CDO resulted in a U.S. government bailout.[74]

In theory, because credit default swaps are two-party contracts, there is no net loss of wealth. For every company that takes a loss, there will be a corresponding gain elsewhere. The question is which companies will be on the hook to make payments and take losses, and will they have the funds to cover such losses. When investment bank Lehman birodarlar went bankrupt in September 2008, it created a great deal of uncertainty regarding which financial institutions would be required to pay off CDS contracts on its $600 billion in outstanding debts.[75][76] Significant losses at investment bank Merrill Lynch due to "sintetik CDO " (which combine CDO and CDS risk characteristics) played a prominent role in its takeover by Bank of America.[77]

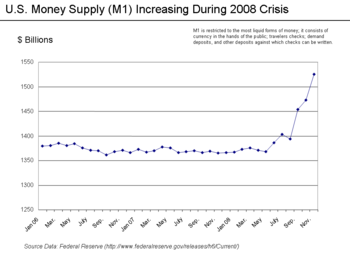

Effect on the Money Supply

One measure of the availability of funds (liquidity) can be measured by the pul ta'minoti. During late 2008, the most liquid measurement of the U.S. money supply (M1) increased significantly as the government intervened to inject funds into the system.

The focus on managing the money supply has been de-emphasized in recent history as inflation has moderated in developed countries. Historically, a sudden increase in the money supply might result in an increase in interest rates to ward off inflation or inflationary expectations.[78]

Should the U.S. government create large quantities of money to help it purchase toxic mortgage-backed securities and other poorly-performing assets from banks, there is risk of inflation and dollar devaluation relative to other countries. However, this risk is of less concern to the Fed than deflation and stagnating growth as of December 2008.[79] Further, the dollar has strengthened as other countries have lowered their own interest rates during the crisis. This is because demand for a currency is typically proportional to interest rates; lowering interest rates lowers demand for a currency and thus it declines relative to other currencies.

During a January 2009 speech, Fed Chairman Ben Bernanke described the strategy of lending against various types of collateral as "Credit Easing" and explained the risks of inflation as follows: "Some observers have expressed the concern that, by expanding its balance sheet, the Federal Reserve is effectively printing money, an action that will ultimately be inflationary. The Fed's lending activities have indeed resulted in a large increase in the excess reserves held by banks. Bank reserves, together with currency, make up the narrowest definition of money, the monetary base; as you would expect, this measure of money has risen significantly as the Fed's balance sheet has expanded. However, banks are choosing to leave the great bulk of their excess reserves idle, in most cases on deposit with the Fed. Consequently, the rates of growth of broader monetary aggregates, such as M1 and M2, have been much lower than that of the monetary base. At this point, with global economic activity weak and commodity prices at low levels, we see little risk of inflation in the near term; indeed, we expect inflation to continue to moderate."[16]

Vicious Cycles

Cycle One: Housing Market

Birinchi yomon tsikl is within the housing market and relates to the feedback effects of payment delinquencies and foreclosures on home prices. By September 2008, average U.S. housing prices had declined by over 20% from their mid-2006 peak.[80][81]

This major and unexpected decline in house prices meant that many borrowers have zero or salbiy kapital in their homes, meaning their homes were worth less than their mortgages. As of March 2008, an estimated 8.8 million borrowers — 10.8% of all homeowners — had negative equity in their homes, a number that is believed to have risen to 12 million by November 2008. Borrowers in this situation have an incentive to "walk away" from their mortgages and abandon their homes, even though doing so will damage their credit rating for a number of years.[82]

The reason is that unlike what is the case in most other countries, American residential mortgages are non-recourse loans; once the creditor has regained the property purchased with a mortgage in default, he has no further claim against the defaulting borrower's income or assets. As more borrowers stop paying their mortgage payments, foreclosures and the supply of homes for sale increase. This places downward pressure on housing prices, which further lowers homeowners' tenglik. The decline in mortgage payments also reduces the value of ipoteka kreditlari bilan ta'minlangan qimmatli qog'ozlar, which erodes the net worth and financial health of banks. Bu yomon tsikl is at the heart of the crisis.[83]

Cycle Two: Financial Market and Feedback into Housing Market

The second vicious cycle is between the housing market and financial market. Foreclosures reduce the cash flowing into banks and the value of mortgage-backed securities (MBS) widely held by banks. Banks incur losses and require additional funds (“recapitalization”). If banks are not capitalized sufficiently to lend, economic activity slows and unemployment increases, which further increases foreclosures.

2008 yil avgust holatiga ko'ra moliyaviy firmalar around the globe have written down their holdings of subprime related securities by US$501 billion.[84] Mortgage defaults and provisions for future defaults caused profits at the 8533 USA depozit muassasalari insured by the FDIC to decline from $35.2 billion in 2006 Q4 billion to $646 million in the same quarter a year later, a decline of 98%. 2007 Q4 saw the worst bank and thrift quarterly performance since 1990. In all of 2007, insured depository institutions earned approximately $100 billion, down 31% from a record profit of $145 billion in 2006. Profits declined from $35.6 billion in 2007 Q1 to $19.3 billion in 2008 Q1, a decline of 46%.[85][86]

Federal zaxira data indicates banks have significantly tightened lending standards throughout the crisis.[87]

Understanding the shadow banking system

A variety of non-bank entities have emerged through moliyaviy yangilik over the past two decades to become a critical part of the credit markets. These entities are often intermediaries between banks or corporate borrowers and investors and are called the soya bank tizimi. These entities were not subject to the same disclosure requirements and capital requirements as traditional banks. As a result, they became highly leveraged while making risky bets, creating what critics have called a significant vulnerability in the underpinnings of the financial system.

These entities also borrowed short-term, meaning they had to go back to the proverbial well frequently for additional funds, while purchasing long-term, illiquid (hard to sell) assets. When the crisis hit and they could no longer obtain short-term financing, they were forced to sell these long-term assets into very depressed markets at fire-sale prices, making credit more difficult to obtain system-wide. 1998 yil Uzoq muddatli kapitalni boshqarish crisis was a precursor to this aspect of the current crisis, as a highly leveraged shadow banking entity with systemic implications collapsed during that crisis.

In a June 2008 speech, U.S. Treasury Secretary Timoti Geytner, then President and CEO of the NY Federal Reserve Bank, placed significant blame for the freezing of credit markets on a "run" on the entities in the "parallel" banking system, also called the soya bank tizimi. These entities became critical to the credit markets underpinning the financial system, but were not subject to the same regulatory controls. Further, these entities were vulnerable because they borrowed short-term in liquid markets to purchase long-term, illiquid and risky assets. This meant that disruptions in credit markets would make them subject to rapid dam olish, selling their long-term assets at depressed prices.[88]

He described the significance of these entities: "In early 2007, asset-backed commercial paper conduits, in structured investment vehicles, in auction-rate preferred securities, tender option bonds and variable rate demand notes, had a combined asset size of roughly $2.2 trillion. Assets financed overnight in triparty repo grew to $2.5 trillion. Assets held in hedge funds grew to roughly $1.8 trillion. The combined balance sheets of the then five major investment banks totaled $4 trillion. In comparison, the total assets of the top five bank holding companies in the United States at that point were just over $6 trillion, and total assets of the entire banking system were about $10 trillion." He stated that the "combined effect of these factors was a financial system vulnerable to self-reinforcing asset price and credit cycles."[88]

Nobel laureate economist Pol Krugman described the run on the shadow banking system as the "core of what happened" to cause the crisis. "As the shadow banking system expanded to rival or even surpass conventional banking in importance, politicians and government officials should have realized that they were re-creating the kind of financial vulnerability that made the Great Depression possible—and they should have responded by extending regulations and the financial safety net to cover these new institutions. Influential figures should have proclaimed a simple rule: anything that does what a bank does, anything that has to be rescued in crises the way banks are, should be regulated like a bank." He referred to this lack of controls as "malign neglect."[89]

Adabiyotlar

- ^ FDIC-Guidance for Subprime Lending

- ^ President's Address to the Nation

- ^ Maklin, Betani va Djo Nocera, Hamma shaytonlar bu erda: moliyaviy inqirozning yashirin tarixi Portfolio, Penguin, 2010, p.82, 83, 86, 89, 144

- ^ Resisting Corporate Corruption: Cases in Practical Ethics From Enron Through ... | By Stephen V. Arbogast| Vili

- ^ Moliyaviy inqirozni tekshirish bo'yicha hisobot, p.74-75

- ^ McLean, Bethany and Joe Nocera, Barcha shaytonlar bu erda, moliyaviy inqirozning yashirin tarixi Portfolio, Penguin, 2010, p.144

- ^ Katta qisqa, Michael Lewis, p.23

- ^ a b v Have Wall Street banks gone subprime at the wrong time?

- ^ Frontline-Inside the Meltdown

- ^ Wachovia & Wamu

- ^ a b v Frontline - Inside the Meltdown

- ^ Roubini-10 Risks to Global Growth

- ^ Friedman, Thomas L. (2008-11-16). "Gonna Need a Bigger Boat". The New York Times. Olingan 2010-05-24.

- ^ Greenspan Op Ed WSJ

- ^ a b Roubini - More Doom Ahead

- ^ a b Bernanke Speech - January 13 2009

- ^ NYT Friedman - We're Gonna Need a Bigger Boat

- ^ "Subprime tartibsizlik qanchalik og'ir?". NBC News. Associated Press. 2007-03-13. Olingan 2008-07-13.

- ^ Ben S. Bernanke (2007-05-17). The Subprime Mortgage Market (Nutq). Chikago, Illinoys. Olingan 2008-07-13.

- ^ Ben S. Bernanke (2007-10-17). The Recent Financial Turmoil and its Economic and Policy Consequences (Nutq). Nyu-York, Nyu-York. Olingan 2008-07-13.

- ^ Ben S. Bernanke (2008-01-10). Financial Markets, the Economic Outlook, and Monetary Policy (Nutq). Vashington, Kolumbiya Olingan 2008-06-05.

- ^ Bernanke, Ben S (2008-05-05). Mortgage Delinquencies and Foreclosures (Nutq). Columbia Business School's 32nd Annual Dinner, New York, New York. Olingan 2008-05-19.CS1 tarmog'i: joylashuvi (havola)

- ^ [1]

- ^ Harvard Report Arxivlandi 2010-06-30 at the Orqaga qaytish mashinasi

- ^ "Delinquencies and Foreclosures Increase in Latest MBA National Delinquency Survey" (Matbuot xabari). Mortgage Bankers Association. 2007-06-12. Arxivlandi asl nusxasi 2008-06-18. Olingan 2008-07-13.

- ^ "U.S. FORECLOSURE ACTIVITY INCREASES 75 PERCENT IN 2007". RealtyTrac. 2008-01-29. Olingan 2008-06-06.

- ^ Realty Trac-2008 Data

- ^ CNN - Realty Trac Data

- ^ NY Post - The Foreclosure Five

- ^ Realty-Trac 2008 Foreclosure Report

- ^ NY Times

- ^ MBA Survey Arxivlandi 2013-05-14 da Orqaga qaytish mashinasi

- ^ Christie, Les (2007-10-17). "ARM resets peaking: Borrowers unprepared - Oct. 17, 2007". CNN. Olingan 2008-05-19. Sana qiymatlarini tekshiring:

| yil = / | sana = mos kelmaslik(Yordam bering) - ^ "FRB: Testimony--Chairman Bernanke on the economic situation and outlook--8 November 2007". 2008. Olingan 2008-05-19.

- ^ Negative Equity

- ^ "New home sales fell by record amount in 2007 - Real estate - NBC News". 2008. Olingan 2008-05-19.

- ^ "Housing Meltdown". 2008. Olingan 2008-05-19.

- ^ Vacant homes 2.9MM

- ^ "America's economy – Getting worried downtown". Iqtisodchi. 2007-11-15. Olingan 2008-05-19. Sana qiymatlarini tekshiring:

| yil = / | sana = mos kelmaslik(Yordam bering) - ^ Case Shiller Data File

- ^ Case Shiller Index May 2008

- ^ a b FT-Wolf Japan's Lessons

- ^ Bureau of Economic Analysis - Personal Savings Chart

- ^ Lasch, Christopher. "The Culture of Consumerism". Iste'molchilik. Smithsonian Center for Education and Museum Studies. p. 1. Olingan 2008-09-15.

- ^ Iqtisodiy tahlil byurosi, NIPA, Table 2.9, 100 - line 46.

- ^ Iqtisodiy tahlil byurosi, NIPA, Table 7.12, line 90.

- ^ Z.1 Historical Tables (1974) va current Z.1 release (2008), Table B.100, lines 31,48.

- ^ "Zakaria: A More Disciplined America | Newsweek Business | Newsweek.com". Newsweek.com. Olingan 2008-10-24.

- ^ Fortune-The $4 trillion housing headache

- ^ Board of Governors of the Federal Reserve System, Release Z.1, 9/19/08. Table 218, lines 2, 11-13, 18, 19. At midyear 2008, securitized home equity loans amounted to a mere $56 billion (line 26).

- ^ a b Staff writer (9 October 2008). "Special report: The world economy: When fortune frowned". Iqtisodchi. Olingan 24 oktyabr 2008.

- ^ a b Blackburn, Robin (March–April 2008). "The Subprime Crisis". Yangi chap sharh. Yangi chap sharh. II (50).CS1 maint: ref = harv (havola)

- ^ "Lessons from the Crisis". pimco.com. PIMCO. 26 Noyabr 2008. Arxivlangan asl nusxasi 2010 yil 27 mayda.

- ^ "FT.com / Video & Audio / Interactive graphics - Credit squeeze explained". 2008. Olingan 2008-05-19.

- ^ Case Study-Mortgage Company Risk Factors

- ^ Daniel Gross (2008-04-01). "The Mark-to-Market Melee". Newsweek. Washington Post kompaniyasi. Olingan 2008-05-19.

- ^ "Subprime mortgage woes infect commercial paper market - MarketWatch". 2008. Olingan 2008-05-19.

- ^ Neil Unmack (2007-10-18). "Rhinebridge Commercial Paper SIV May Not Repay Debt (Update1)". New York City, United States: Bloomberg L.P. Olingan 2008-07-13.

- ^ "The $2 bail-out". Iqtisodchi. London: Iqtisodchilar guruhi. 2008-03-19. Olingan 2008-05-19.

- ^ PIMCO - Lessons from the Crisis

- ^ "BofA: The Credit Crunch Takes Its Toll". 2008. Olingan 2008-05-19.

- ^ Leverage Info

- ^ Business Week - Lehman & Merrill Lynch

- ^ Time Magazine - Financial Madness

- ^ AIG-Fortune Magazine-$150 Billion Was Just the Beginning

- ^ "SIVs, next shoe to drop in global credit crisis? - International Business Times -". 2008. Arxivlangan asl nusxasi 2008-02-25. Olingan 2008-05-19.

- ^ Blackburn - Subprime crisis

- ^ Roubini-The U.S. Financial System is Effectively Insolvent-March 2009

- ^ Fox News - E Mac Discussion of Citibank

- ^ a b WSJ Article - Bailout of Money Funds

- ^ Diya Gullapalli and Shefali Anand. Bailout of Money Funds Seems to Stanch Outflow. The Wall Street Journal. Bozorlar. 2008-09-20. Retrieved 2008-09-25

- ^ WSJ Article

- ^ Markewatch Article - LIBOR Jumps to Record

- ^ a b Bloomberg-Credit Swap Disclosure Obscures True Financial Risk

- ^ AP - Lehman Debt Auction Gives Clue to Potential Losses

- ^ Lehman 10Q May 08

- ^ NYT - How the Thundering Herd Faltered and Fell

- ^ Fed-Money Supply Explanation

- ^ Fed Release December 16

- ^ Case Shiller Index

- ^ Economist-A Helping Hand to Homeowners

- ^ Endryus, Edmund L.; Uchitelle, Lui (2008-02-22). "Negative Equity". The New York Times. Olingan 2010-05-24.

- ^ NYT - How to Help People Whose Homes are Underwater

- ^ "Bloomberg.com: Butun dunyo bo'ylab". Bloomberg.com. Olingan 2008-10-26.

- ^ "FDIC Quarterly Profile Q1 08" (PDF). Arxivlandi asl nusxasi (PDF) 2012-06-07 da.

- ^ "FDIC Profile FY 2007 Pre-Adjustment" (PDF). Arxivlandi asl nusxasi (PDF) 2012-06-07 da.

- ^ Banks Tighten Lending Standards

- ^ a b Geithner-Speech Reducing Systemic Risk in a Dynamic Financial System

- ^ Krugman, Pol (2009). Depressiya iqtisodiyotining qaytishi va 2008 yildagi inqiroz. VW. Norton Company Limited. ISBN 978-0-393-07101-6.

Tashqi havolalar

- PBS Frontline - Inside the Meltdown

- Schneiderman, R.M; Philip Caulfield; Celena Fang; Elisabeth Goodridge; Vikas Bajaj (2008-09-15). "How a Market Crisis Unfolded: Some of the key events in the upheaval". Nyu-York Tayms. Olingan 2008-09-17. (Graphic and interactive timeline.)

- Kuper, Jorj (2008). The Origin of Financial Crises: Central banks, credit bubbles and the efficient market fallacy. Petersfield, Hampshire, U.K.: Harriman House. p. 208. ISBN 978-1-905641-85-7.

- "Fannie, Freddie and Henry". Wall Street Journal. 2008-09-09. Olingan 2008-09-09. (Interactive timeline of Treasury Secretary Paulson's changing policy actions in relation to Fannie Mae and Freddie Mac – requires Chiroq.)

- Milken Institute, Demystifying the Mortgage Meltdown: Slideshow, 2008 yil 2 oktyabr.